Budgeting Family Finances – Step by Step Guide for Families to Create Perfect Family Budget

Introduction to the steps to step budgeting guide

Budgeting would help people to spend less, save more and unnecessary money loses such as late payments of utility bills, loans and/or credit cards.

When advising the importance of budgeting finances, financial experts emphasize that budgeting is the best way to get full control over money to a great extent!

Creating a family budget is not a tough task as most of us think. But it is a straightforward activity. Any individual can make a perfect budget at any time. Find below an example with the the step by step guide to budgeting finances in a disciplined way.

The core of building budget is, documenting the income and expenses in a structured order to attain financial discipline and adjusting spending to attain a better financial footing.

This article provides an insight to create and maintain your own family budget.

Before moving to the next step, I would like to inform the major advantages of having a good family budget. This has been discussed in my previous articles as well. Even though, I prefer to re-write the points once again here for late comers to this blog.

- Budgeting gives you control over your money to a great extent.

- Keeps you focused on your financial goals

- Makes you aware what is going on with your money

- Helps you organize your spending and savings

- Makes you decide things in advance

- Enables you to save for expected and unexpected costs

- Provides you with an early warning for potential financial problems

- Helps you determine if you can take debt and how much

- Enables you to produce extra money by avoiding late fees, penalties etc.

- Budgeting also makes you to take control over your debts

- Quality of your life and financial status would improve to great extend

Set Your First Family Budget – Step by Step

Being said, budgeting required to document the income and expense for an identified period of time. To do so, use a convenient method such as using a pen and paper or an Excel sheet or any other comfortable methods.

There are many free and easy online tools and apps are available to prepare and track the budget.

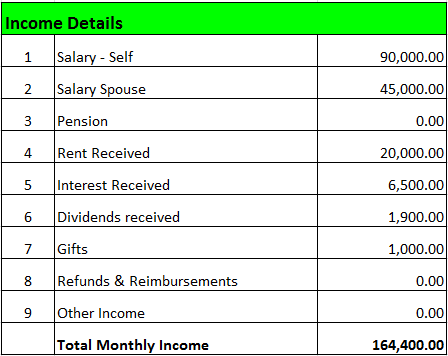

The income parts

Any budget should have two sections. First column is about the income part. In this section, add all the identified income for a month. It can be anything, but ensure this section have populated with intact details.

Here is a sample income column to know this in a better way:

Above mentioned is a sample income report and amend the same by adding or removing any other source of income you have.

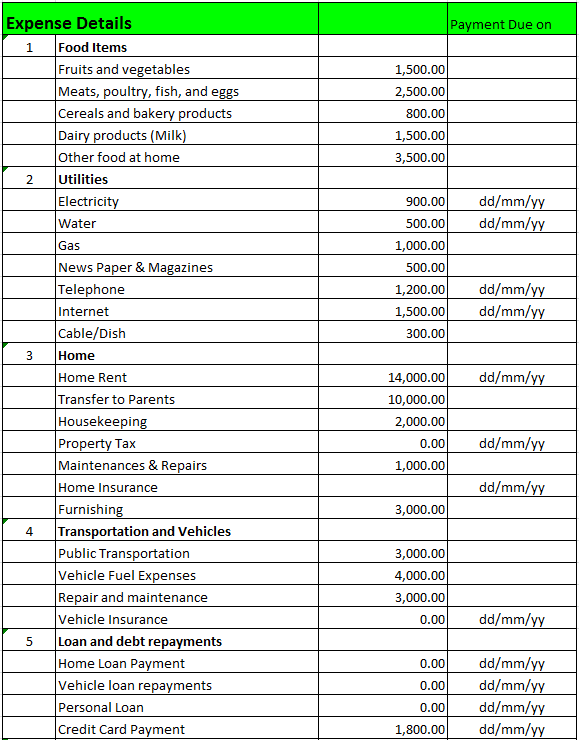

The Expense Part

Once after completed by identifying and listing all the income for the month, it is now the turn for identifying and listing all monthly expenses.

Remember, there are enough possibilities to forget few expense details in this section. It is quite natural.

In order to deal with such unidentified expenses, the best practices are to allocate a percentage of funds under a title of ‘miscellaneous expenses”.

Here is how one can identify and list all the family expenses for a month:

- Always list your regular essentials such as food items, grocery expenses etc.

- Document all the regular monthly expenses such as electricity, gas etc.

- Input home expenses such as rent, appliances, maintenance etc. You can add all the maintenance expenses for home, appliances in this section.

- Transportation and the vehicle maintenance cost comes to in this section

- Have a section for Loan and debt repayments such as vehicle, home loan, personal loans etc.

- Must have a section for kids and their expenses like school fees, babysitting etc.

- Personal expenses appears here and it may vary. These expenses are adjustable later if required, if required.

- Mention the savings and investments in the investment section.

- Give importance to set up an emergency fund aside to meet any unexpected expenses that have forgotten to add in the budget.

To not miss any payments such as utilities, loans, credit cards, have a separate column with payment due date mentioned. This would make sure that not missing any last date and inviting any penalty or interest hike due to late payments.

Below is a sample expense details you can refer. However, there are several columns that are optional. Take this as a model sheet to prepare own list by providing actual expenses in each section.

Once done with budgeting, you will now have a detailed information on total income as well as expenses. There few points to remember:

- Deducting expenses from the total income would give either excess money to hand or more money required to meet the expenses.

- If excess money found, plan with that money. It can either add to the saving or utilize for better purposes such as paying out loans, debts etc.

- If the expenses are more than your income, identify the areas where the necessary changes can be made to reduce expenses.

What is next?

Hope, the step by step guide to budgeting finances helped you to understand the core of budgeting. However, creating a budget itself would not provide required financial safety. There is still few necessary homework to do.

- Each week, add the expenses happening on each item to understand how much the actual spending against the budgeted amount is. If the expenses are higher than the planned amount of any item, take necessary action to trim unnecessary expenses.

- If any expenses are fixed during the budget preparation and there was a hike in pay later, budget also needs to be adjusted accordingly. Loan payments, utility bills are the best examples for this scenario.

- Never think post budgeting balance amount in hand is ‘free money’. But such balances should go to savings and investments for future. A common goal of the budgeting finance itself to save money by adding necessary controls. Each penny in your hand should spend for good purposes.

You may find some missing points in the above article and chart due to the geographic differences. If so, adjust it in a better way to the income and expense charts to make a great budget for self and family.

Happy budgeting!!